This paper highlights some of the key issues for Australia’s superannuation funds when it comes to valuation of private credit and the wider private markets asset class:

- What represents best practice for valuation of private market assets?

- How should the valuation governance of a private market portfolio by assessed?

- What have ASIC and APRA recommended as good or best practice for investing and governing valuation of private market assets which, by their very nature, do not trade in deep secondary markets?

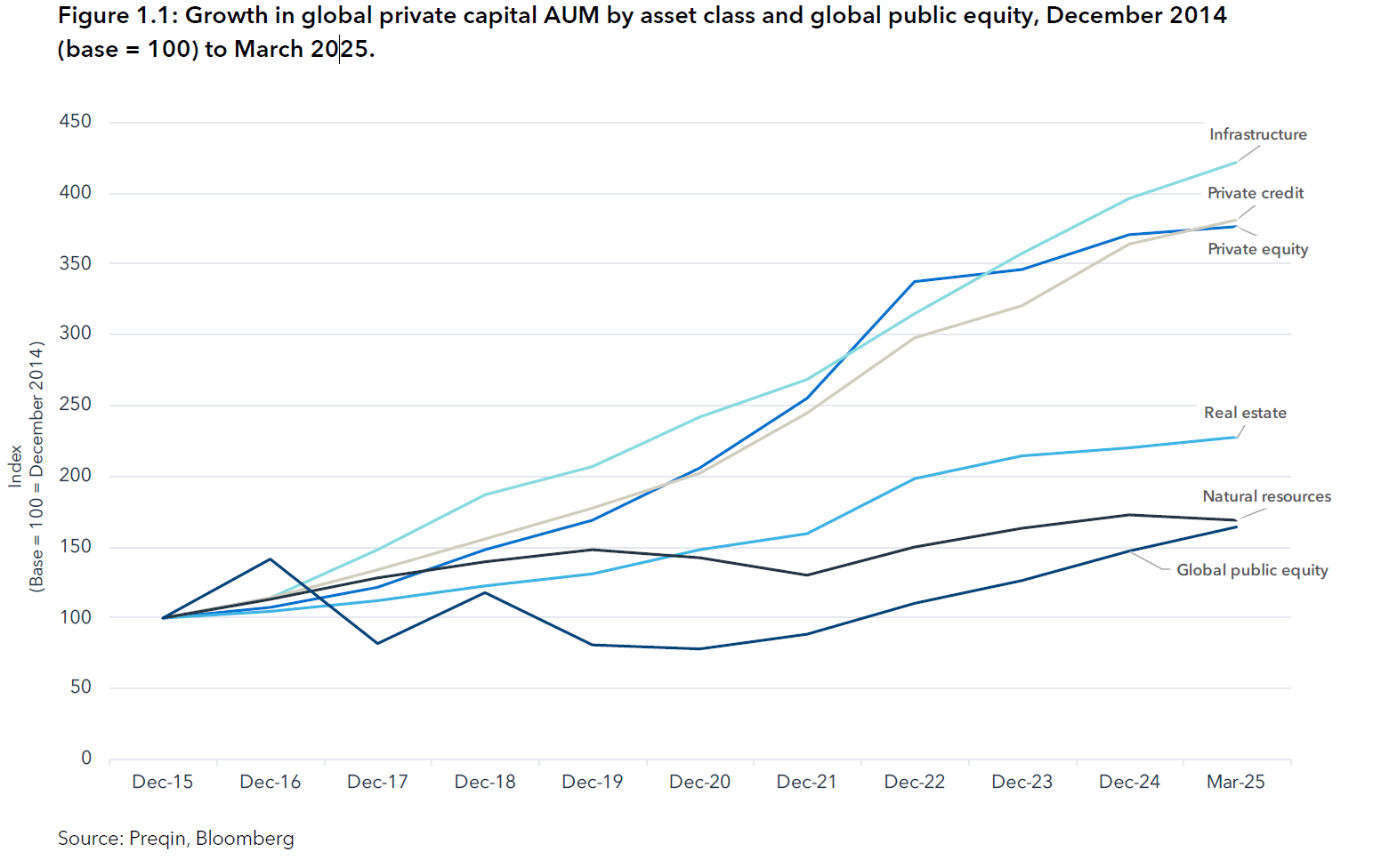

Rapid growth in private credit markets

The confluence of several factors have seen significant growth in investment by public offer super funds in private credit in Australia and around the world.

ASIC’s paper REP823 sets out the growth across all private markets. Within private market assets, private credit has grown nearly 400% over the ten years to June 2025 compared with a mere 50% in global public equity (listed shares).

A difficulty for investors in all private market assets of all types and sizes is the absence of a market price by which mark-to-market valuations of private market assets can be undertaken.

The super fund industry turns to expert, independent valuation firms to provide confidence in the value of private market assets and this has led to a focus on the globally recognised International Valuation Standards Council and its International Valuation Standards.

Together with oversight by APRA and ASIC, Australia is fortunate to have sophisticated guardrails for public offer super funds which choose to invest directly or via managers in the private credit market.

What represents best practice for valuation of private credit investments?

The International Valuation Standards Council (IVSC) recommends using the International Valuation Standards (IVS), particularly IVS 500: Financial Instruments, for the valuation of private credit.

Effective from January 2025, the updated International Valuation Standards emphasise a fair value approach focused on market-driven, observable inputs, combined with professional judgment.

An exposure draft of proposed changes to the relevant general and specific standards is available until 30 April 2026 for public consultation.

Key recommendations from the current IVSC standards for private credit valuation include:

- Primary Valuation Approaches

- Income Approach (Discounted Cash Flow – DCF): Since private debt often lack active market prices, the IVSC highlights the income approach, which converts future cash flows to a single present value.

- Yield Method: A specific type of income approach where valuers estimate expected cash flows, determine a discount rate that reflects credit risk, subordination, and liquidity, and back-test results.

- Market Approach: The preferred approach when reliable, recent transaction data for similar instruments is available.

- Key Components of Private Credit Valuation (IVS 500)

- Calibration: Input parameters should be calibrated to the price at which the investment was made, adjusting for subsequent changes in credit quality and market conditions (e.g., credit spreads).

- Risk Assessment (IVS 500.140): Valuations must account for the specific credit risk (uncertainty of repayment) and liquidity risk inherent in private instruments.

- Discount Rate Determination: The required return should reflect the market participant view of risk-free rates plus a risk premium, often calculated via internal rate of return (IRR) or a build-up method.

- Procedural Best Practices (IVS 104, 105, 106)

- Data Quality (IVS 104): Emphasis on verifying borrower data, with professional scepticism applied to management-provided information.

- Modeling (IVS 105): Use of models should be accompanied by clear documentation of assumptions, with professionals retaining responsibility over automated tools.

- Documentation and Transparency (IVS 106): Expanded requirements for documenting key inputs, assumptions, and the rationale behind the valuation.

IVSC also notes that while fair value is the standard for financial reporting, for specific lending contexts, lenders may also look to “Prudential Value” or “Mortgage Lending Value” approaches.

In the context of public offer super funds, both ASIC and APRA encourage the development of valuation governance frameworks which ensure best of breed oversight of investment valuations.

What represents best practice investment portofolio valuation governance?

The prominent global framework for assessing the reliability of investment portfolio valuations is primarily driven by the International Valuation Standards (IVS), developed by the International Valuation Standards Council (IVSC).

These standards are used in over 100 countries to promote consistency, transparency, and accountability across various asset classes, particularly in private markets where valuation reliability is crucial.

Key Components of the Global Framework

The framework consists of several pillars that ensure valuation reliability:

- International Valuation Standards (IVS): Updated regularly (with a 2025 update effective from January 31, 2025), IVS provides a principles-based framework. It covers general standards for valuation conduct (e.g., IVS 104 – Data and Inputs, IVS 105 – Valuation Models, and IVS 106 – Documentation and Reporting).

- IPEV Guidelines: For private capital investments (venture capital, buyouts), the International Private Equity and Venture Capital (IPEV) Valuation Guidelines are widely accepted as best practice, often used in conjunction with IVS.

- Fair Value Hierarchy (IFRS 13/ASC 820): IVS aligns with international accounting standards, including IFRS 13, which requires assets to be categorized into three levels, with Level 3 representing the most unobservable inputs and highest uncertainty.

- Governance Frameworks: Global regulators (like APRA in Australia or the SEC in the US) expect strong internal governance, including independent valuation committees, conflict-of-interest management, and rigorous, proactive revaluation triggers, especially during market volatility.

Assessing Reliability (Best Practices)

To determine if a portfolio valuation is reliable, the following best practices are recognized internationally:

- Independent Valuation Governance: Separate valuation functions from the investment team to avoid conflicts of interest.

- Regular and Rigorous Back-testing: Periodically comparing modelled valuations with actual market transactions to verify model accuracy.

- Proactive Revaluation Triggers: Using both quantitative (e.g., percentage movement in indices) and qualitative (e.g., specific investment news) triggers to prompt out-of-cycle valuations.

- Documentation and Transparency: Maintaining high-quality documentation that supports the assumptions and inputs used in valuation models.

The IVSC works closely with the International Organization of Securities Commissions (IOSCO) to strengthen regulatory confidence in these valuation practices globally.

The ASIC review of private markets assets

ASIC’s 2025 focus on private markets, detailed in reports REP 823 and REP 814, highlights urgent concerns over valuation uncertainty, opacity, and conflicts of interest in private credit and equity. The regulator aims to improve valuation practices, governance, and transparency, ensuring fair treatment of investors as super funds increase allocations.

Key Aspects of ASIC’s Private Market Focus (2025-2026):

- Surveillance of Valuations: ASIC is conducting thematic surveillance of valuation practices, particularly focusing on how private credit and equity funds determine asset values (REP 823).

- REP 814 – Private Credit Surveillance: This report, published in September 2025, investigates 28 retail and wholesale funds, scrutinizing how managers handle risk and valuation.

- Key Risks Identified: Key concerns include lack of transparency (opacity), inherent valuation uncertainty, potential conflicts of interest, illiquidity, and high leverage.

- Regulatory Roadmap (REP 823): Released in November 2025, this report provides a roadmap to address emerging risks in private markets and improve disclosure to investors.

ASIC encourages improved standards for asset valuation and management, particularly for funds targeting retail investors.

ASIC has published the paper Rep823 which includes the following statement:

Valuation: Our findings on financial reporting and audits for registrable superannuation entities Accounting for your super: ASIC’s review into the financial reporting and audit of super funds (REP 816) underscore a clear need to improve confidence in the valuation of unlisted fund assets, including by superannuation trustees and auditors. Findings revealed inconsistent approaches to disclosing investments, limited disclosure of sponsorship and advertising expenses, and insufficient audit evidence obtained in the valuation of unlisted investments. The valuation concern arose when superannuation trustees relied on the information provided by external fund managers. This is a reminder to funds and trustees to ensure rigorous governance over critical investment information such as valuations, given their responsibility for members in private investments.

The APRA review of unlisted asset valuations

APRA’s December 2024 review of unlisted asset valuations found improved trustee capability in valuation and liquidity risk governance, yet identified material gaps in valuation practices for a significant proportion of superannuation trustees. APRA expects enhanced, timely revaluation processes, with a focus on strengthening revaluation triggers.

Key Findings from APRA’s 2024 Review

- Coverage: The review covered Unlisted Property, Unlisted Infrastructure, Unlisted Equity, and Private Debt.

- Observations: While some trustees showed better practices—including embedding valuation risks in audits—many fell short in establishing robust, ongoing revaluation triggers.

- Next Steps: APRA is directly engaging with trustees identified as having deficiencies and expects improved, proactive remediation plans regarding their valuation frameworks.

Key APRA Publications and Guides

- December 2024 Review: Governance of Unlisted Asset Valuation and Liquidity Risk Management in Superannuation.

- Self-Assessment Survey (June 2024): Observations from SPS 530 – Valuation Governance Framework Self-Assessment Survey.

- Prudential Practice Guide: SPG 531 – Valuation provides guidance on how to manage valuation frequency, especially for private equity.

These findings complement ongoing ASIC efforts to ensure adequate valuation oversight of private markets in Australia’s evolving capital landscape.

Item 15 of the Prudential Practice Guide 531 states that every RSE licensee should have a written policy on valuations, viz:

Valuation policy and procedures

15. APRA expects that an RSE licensee would have a formally documented valuation policy approved by the Board that outlines the RSE licensee’s valuation procedures.

APRA’s Prudential Practice Guide 530 at page 32, Valuation, sets out what APRA expects of RSE Licensees in terms of valuation policy and governance.

It is important that RSE licensees establish a basis for tracking valuation approaches, sources of inputs as proposed on page 33:

Valuation methodology

40. c) the valuation methodology employed for each asset class (and sub-asset class and instrument/holding vehicle type where relevant), including the sources of valuation inputs;

Similarly, APRA encourages the RSE Licensee to form a view on when external valuations should be obtained:

Independent external valuations

40. d) the circumstances under which independent external valuations are to be obtained;

Peloton has decades of experience working with investment managers, advisers, superannuation funds and investee businesses delivering recurring valautions and due diligence.

There has been significant improvement in the overall awareness and adoption of best practice valuation frameworks in the last ten years. However, the pace of growth in the sector means that many funds find it difficult to devote the level of attention that the allocation of funds warrants.

Peloton is here to help. We are always happy to provide some advice, review a policy or consider a valuation challenge.

Email us at helpme@peloton.group if you have a question you would like us to consider!